What is the Kleinunternehmer limit?

Read in 3 minutes

When you are self-employed on a part-time basis, or you are just starting your own business, you may be able to register as a Kleinunternehmer (small business owner) in Germany.

This regulation saves a lot of paperwork and simplifies tax obligations. But when can you – and should you – actually make use of the Kleinunternehmer rule? Here you find everything about the limit for Kleinunternehmer.

How much can you earn as Kleinunternehmer?

When you don’t have more turnover than 22,000€ in the first year of your self-employment and not more than 50,000€ in the following year, you can register as a Kleinunternehmer.

It also applies, when you are self-employed for several years now and you don’t exceed the limit of 22.000€ in the current year (and will not exceed 50.000€ in the next year).

Note that your turnover is not your profit. The turnover is the amount before you deduct your expenses.

Important: If you become self-employed for the first time, note that the 22,000€ refers to the entire calendar year. If you start your own business in the middle of the year, you will have to extrapolate your estimated sales for the whole year.

Example: If you become self-employed in June and want to make use of the Kleinunternehmer rule, you should be sure that you do not exceed €12,833 in the following months until the end of the year. Because the 22.000€ count for the whole calendar year.

Tip from Accountable💡: Even though the Kleinunternehmer rule has some advantages, it can also make sense not to apply for it. It could be more beneficial to voluntarily register as subject to VAT.

For example, if you register an expensive photovoltaic system. In this case you could get back the VAT, which is not a small amount.

How much am I allowed to earn as a Kleinunternehmer?

The Kleinunternehmer rule is only relevant for revenue from your self-employment. If you also work as an employee, for example, the money you make with this job is not taken into account for the Kleinunternehmer rule.

So it doesn’t matter how much you earn as an employee, but it’s different if you have several self-employed businesses at the same time. In this case, your turnovers from self-employment are all added together and taken into account as one sum. Should you earn more than 22,000€ with all your self-employed jobs combined, you can’t be a Kleinunternehmer.

Example: Let’s say you are employed as teacher but also sell homemade jewelry through an online store on the side. In this case, you only need to consider the sales from the online store when wanting to register as Kleinunternehmer.

At the same time a self-employed craftsman who also runs an online store on the side has to add up his sales from both activities and calculate the total, if he is considering whether he can register as a Kleinunternehmer.

This revenue doesn’t count into your total turnover:

For example, if you have clients in other EU countries who fall under the Reverse Charge regulation, you don’t have to take this into account for your turnover. Also, you don’t have to include other tax-exempt income, e.g. medical treatment or some educational and teaching services, as well as income from renting out apartments.

When am I not a Kleinunternehmer anymore?

If you notice that your revenue exceeds the turnover limit, you must change to the standard taxation and are subject to VAT. So it’s important that you keep a close eye on your sales when you reach this limit. Because as soon as you exceed 22,000€, you’re no longer a Kleinunternehmer. You’ll have to charge VAT in your invoices starting from the next year and also pay it to the state.

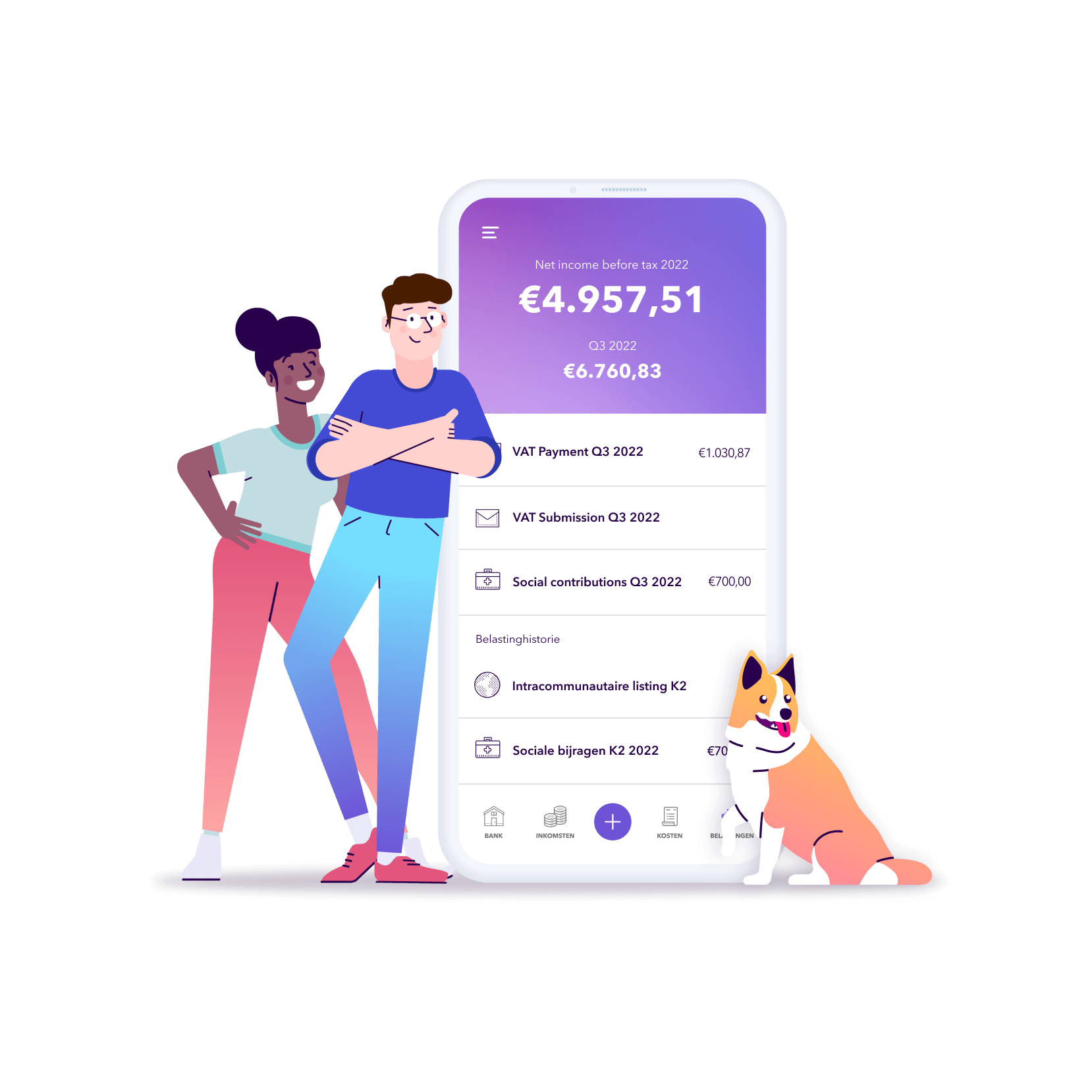

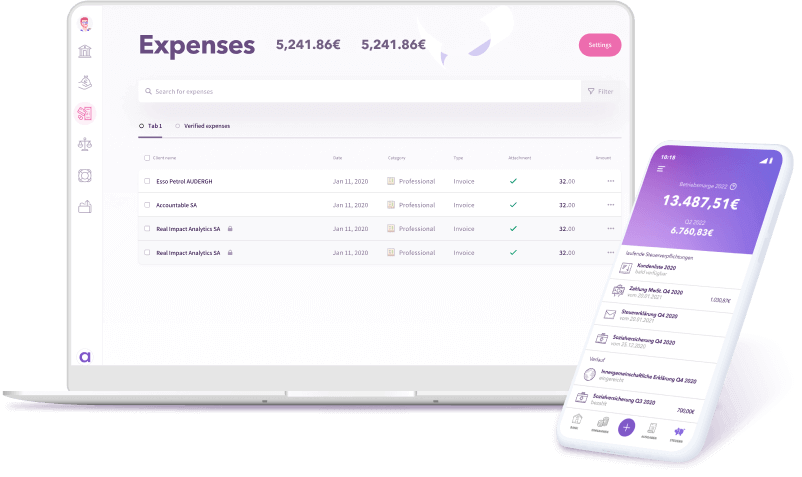

Tip from Accountable💡: If you’re a Kleinunternehmer but might exceed the limit, Accountable is there for you! The Accountable app shows you exactly what you’ve earned and notifies you when you’re about to exceed the 22,000€ threshold!

Did you find what you were looking for?

Happy to hear!

Stay in the know! Leave your email to get notified about updates and our latest tips for freelancers like you.

We’re sorry to hear that.

Can you specify why this article wasn’t helpful for you?

Thank you for your response. 💜

We value your feedback and will use it to optimise our content.

This is how you can use Accountable for your taxes!

What other freelancers are reading

Sophia loves literature and writing. She's happy to have joined the Accountable team and is becoming a pro on all things tax related.

In her free time you will find her in a boulder gym, studying Italian or discovering the streets of her new hometown Berlin.