| Age | Public Health Insurance (14% of Income) | Private Health Insurance (Minimum Coverage) | Private Health Insurance (Premium Coverage) |

|---|---|---|---|

| 26 years old | €198 – €918 | €223 – €859 | Higher than €859 |

| 56 years old | €198 – €918 | €503 – €1,402 | Higher than €1,402 |

You are thinking of starting out as a self-employed professional in Germany? You have come to the right place! Here you find the free resources to answer all essential questions to become self-employed.

On this page you will find everything you need to successfully master the path to self-employment. From the initial idea to the legal and tax aspects through to practical implementation, you will receive valuable information and advice.

Before you register as a self-employed, you need a solid understanding of the differences compared to a job as an employee and how exactly you want to build your business. Here we answer the most difficult questions most people ask our Tax Coaches.

Before you start, you should have developed a clear business idea. Have your offer clearly defined and know who your ideal target audience is. You might also have to research the regulations and specific permits or licenses for your business type.

Also, know what financial resources you need to get your business off the ground. Remember that next to business expenses you will need to set aside money for insurance costs and taxes. With software like Accountable, you always see how much you earn and how much taxes you have to pay.

Then, you will have to register your business with the tax office and apply for a tax number.

In most cases, you can start as a self-employed professional without a specific degree or qualifications.

However, some professions, like doctors or lawyers, require specific degrees and professional qualifications. Others, such as web designers or consultants, may not require formal qualifications, but having relevant skills, experience, and certifications can enhance your credibility and competitiveness.

There is no fixed amount required by law to start as a self-employed individual in Germany, but you should have enough capital to cover your initial business expenses, including registration fees, office space, living expenses, and taxes. Here are some potential sources of funding and support:

Yes, you can generally start a self-employed part-time job while being employed at the same time. But before you do:

Yes, generally it is totally possible to become self-employed if you were previously unemployed. Also, it can be difficult to finance your start into self-employment. Therefore you can apply for the Gründungszuschuss (start-up subsidy) or the Einstiegsgeld (introductory grant), to receive financial support so that you can successfully become self-employed from unemployment.

Consider that, if you are receiving unemployment benefits (Arbeitslosengeld I) and you register a self-employed business, you are typically no longer seen as unemployed, and your benefits may be adjusted or suspended.

Also, if you receive Arbeitslosengeld II, also known as Hartz IV, the Arbeitsagentur (Job Center) will assess your business income, and if it’s below a certain threshold, you may still be eligible for some benefits to supplement your income.

In Germany, there are different types of self-employment, depending on the activity and legal status. Here are the most relevant types:

Everybody with the permission to work in Germany can register as a self-employed and start their business. Below we have provided you with a concrete list of the legal steps you have to take. So that you’re set up for success right from the start!

What is it?

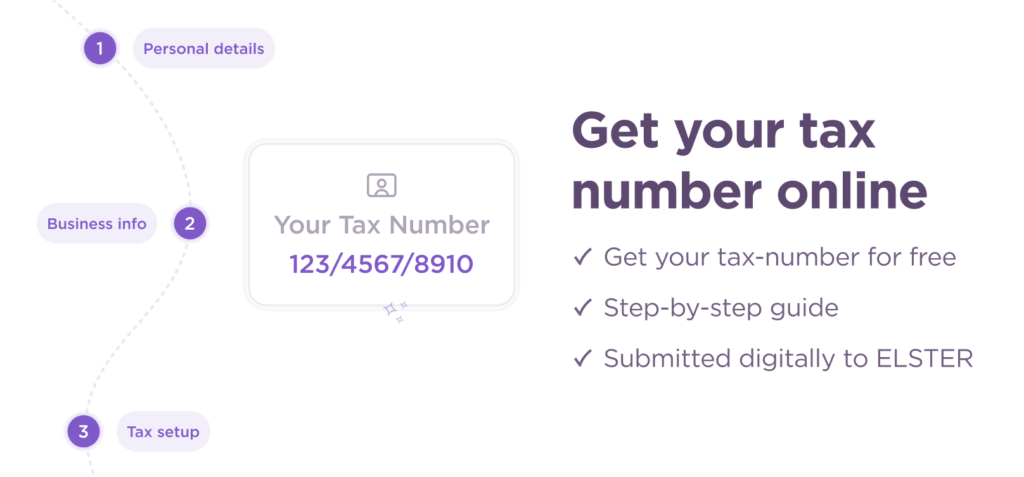

It’s necessary to obtain your tax identification number (Steuernummer) which allows you to invoice clients and officially conduct business.

Do I really need it?

Yes, it is mandatory for all self-employed professionals. Otherwise, you’re not able to send correct and legal invoices to clients.

Where can I get it and what does it cost?

The official registration with your Finanazmt is free of charge. You can find the digital form online. Either fill it in on the ELSTER or Accountable website. You can also fill it out with the help of a tax advisor. They usulally charge €90 – €150.

What is it?

This registration is required for those who are starting a trade business (Gewerbe). This is the formal act of announcing the commencement of a trade business to the local trade office (Gewerbeamt).

Do I really need it?

It’s only required for those operating a trade business (Gewerbe). Freelancers (Freiberufler) are exempt. Find out if you are Gewerbe or Freiberufler here.

Where can I get it and what does it cost?

You can obtain the Gewerbeanmeldung at the trade office of your local municipality. Larger cities might have multiple offices, so it’s best to check in advance which one is responsible for your district or area. Costs vary between €20 – €60.

What is it?

It’s the registration with the commercial register for business entities (Handelsregisteranmeldung). Generally, individual self-employed professionals don’t need to register.

Do I really need it?

No, not necessary for most self-employed individuals. It’s more relevant for larger business entities like GmbH or UG.

Where can I get it and what does it cost?

The Handelsregister is maintained by the local Amtsgericht. The exact court and the department responsible for it may vary depending on your location. Costs for self-employed professionals should be around €20 – €30 for the registration if you don’t consult a lawyer or tax advisor.

What is it?

Depending on the nature of your business, additional permits might be necessary. Examples could be health and safety permits, food handling certificates, etc.

Do I really need it?

It varies depending on the type of business and the industry. You might need it for opening a restaurant or a pharmacy, for example.

Where can I get it and what does it cost?

It really depends on what you do. For specific permits and authorizations in Germany, such as those required for certain trades (Gewerbeordnung, Meisterpflicht in crafts) you must consult the relevant professional bodies to determine the exact costs.

The one thing everybody needs to do: register with the tax office (Finanzamt). With this free form you can register officially and free of charge. After submitting the form the Finanzamt will review your registration form and send you your tax number via letter.

Anyone starting a self-employed business in Germany, whether as a freelancer or a tradesperson (Gewerbe), needs to register with the tax office (Finanazmt). This also applies if you want to register as part-time self-employed or Kleinunternehmer.

Simply put, withour a tax number you can’t invoice your client. A tax number is essential for proper tax reporting and invoicing.

Here you find everything you need to know about the German tax numbers.

The form, which is called “Fragebogen zur steuerlichen Erfassung” asks for details about your business, income, and other relevant information. We’ve provided helpers and articles in English to help you at every step!

The final decision lies with the tax office (Finanzamt). However, there are some guidelines that determine, wether your self-employed profession falls is a Gewerbe or the work of a freelancer. We provide helping context in the form itself to give the right information, but you can also read about it here.

Yes, you can use the form on the Accountable website. It will be sent to your local Finanzamt via our official ELSTER interface.

As a self-employed professional in Germany, there is no legal obligation to hire a tax advisor.

In any case, you are responsible for all your own administration, accounting, and tax obligations. Whether you work with a tax advisor depends on your needs and budget.

The official registration itself is directly available online and free of charge.

If you decide to use Accountable as your tax software, our Tax Coaches will be there to answer your questions on a daily basis. Should you need a tax advisor for a certain issue, we will connect you with one of our official tax advisor partners.

Understand how much taxes you will have to pay as a self-employed professional in Germany. Depending on your profession you can chose typical deductible costs and save taxes.

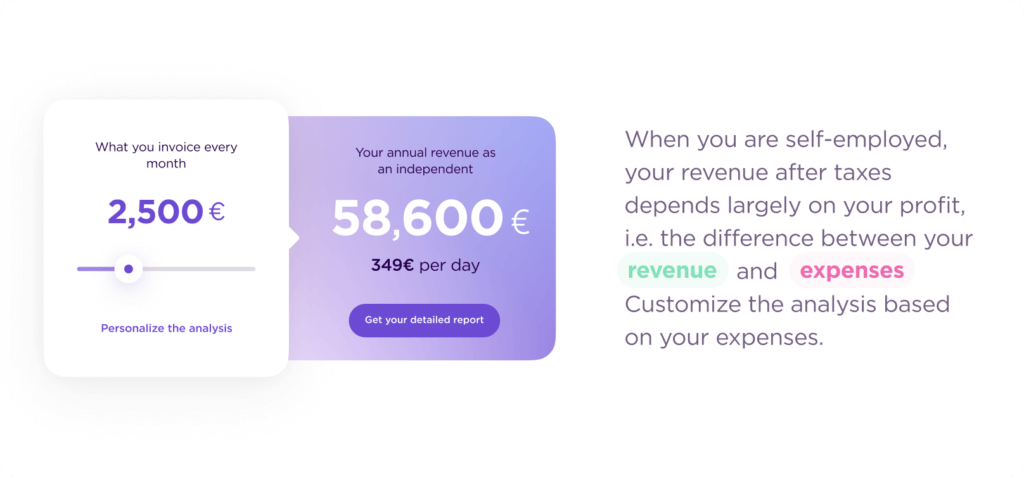

An employee can easily see their net income on their pay slip, while a self-employed individual needs to manually calculate their gross and net income, taking into account various deductions.

Example: Your total monthly costs are €6,000, your working hours are 90 hours a month. Then your hourly rate would have to be at least €66 net to avoid making a loss. However, since you want to make a profit and also have to provide for bad times, you should add a profit markup of at least 10% to your hourly rate.

No, it is often difficult for self-employed professionals to determine their net income without examining their bank statements or estimating based on their revenue and expenses. Here you find our guide on calculating your income.

Let’s take this example to understand how to calculate taxes for self-employed professionals:

You earned €42,000 last year and were able to deduct €2,500 as business expenses. The amount on which you have to pay tax is therefore €39,500.

The income tax rate for this amount is 19%. This corresponds to an income tax liability of €7,663.

But don’t forget that you also have to plan for deductions for social security contributions. This includes at least health insurance and pension insurance, as well as other insurances if applicable.

You can find more about it here.

While health insurance is mandatory, pension insurance is not. However, considering a private pension plan is advised, as relying solely on the state pension may not be sufficient. These are your options.

The taxes you have to pay depend on the amount of your income and the structure of your business:

Every self-employed person must file an income tax return and possibly pay income tax. If you are subject to VAT (value added tax), you have to calculate the VAT and pay it with a regular VAT return. If you have registered as trade person (Gewerbe), you may also have to pay trade tax (Gewerbesteuer).

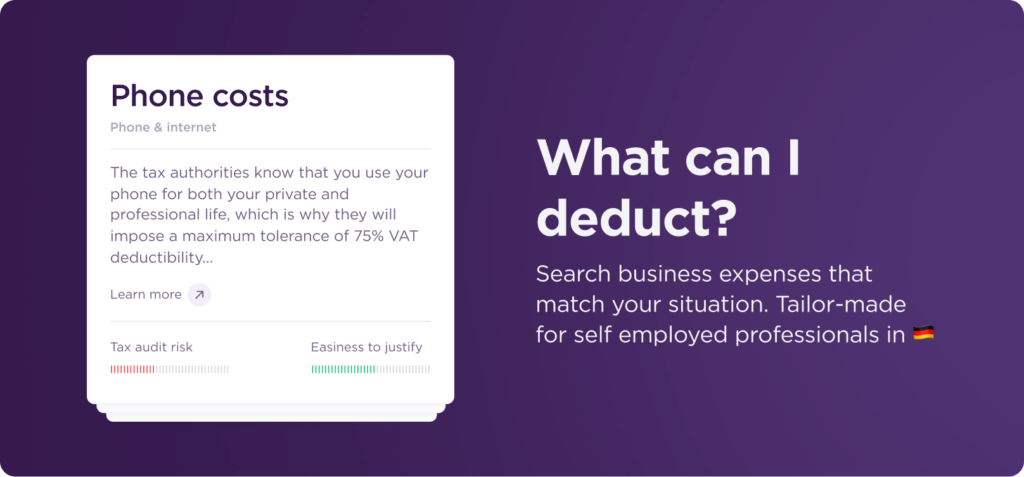

As a self-employed professional, the best way to reduce your taxes is to maximize your business costs, also called deductible expenses. We created this free tool for you, to search all possible deductible expenses in Germany!

Deductible expenses are business-related costs that can be subtracted from your total income. This way, you reduce the income you have to pay taxes on and ultimately reduce the amount of income tax you owe. Some common deductible expenses are:

Here is a list of common deductible expenses for self-employed professionals in Germany:

Yes, there are two ways of deducting your home office. There is the home office lump sum, which allows to deduct €6 per day that you worked at home for 2023. However, the limit here is a maximum of €1,260 per year. So if you have worked more than 210 days in the home office, you can still only deduct 1,260€.

The other possibility is to claim the actual costs for your home office, meaning rent, utilities for your office room etc. In this case, the home office needs to be the main place of work for you.

If you go on a business trip, you can deduct certain costs. These include travel costs, such as a train tickets, hotel accommodation costs, and the additional cost of meals. There is a lump-sum for this, which is called Verpflegungsmehraufwand. With this flat rate, you can deduct €14 per day of arrival and departure and even €28 for each full day.

Generally, you can only deduct costs that are directly related to your business activities. So, if your fitness subscription is primarily for health and personal well-being rather than for business purposes, it is typically not deductible.

You can deduct your car for business purposes, like visiting clients or traveling to business meetings.

There are two main methods for deducting car expenses:

Actual Expenses: You track and deduct the actual costs associated with your car, including fuel, insurance, maintenance, parking fees etc. You need to keep detailed records and receipts for these expenses.

Mileage Allowance Method: This method involves calculating deductions based on the number of kilometers driven for business purposes. You maintain a mileage log (Fahrtenbuch) that records each trip’s date, purpose, starting and ending locations, and mileage. You then apply the standard mileage rate of 30 Cents.

For most self-employed professionals this is one of the highest costs. Here you find guidance on what type of health insurance you can get and how to deduct it.

Unlike employees who are covered through their employers, freelancers and entrepreneurs must arrange their own comprehensive health insurance coverage. There are two options available:

Public Health Insurance in Germany (GKV):

Solidarity system: The GKV is a popular choice because of its “everyone contributes, everyone benefits” approach.

Who’s covered? This system predominantly caters to workers, ensuring a wide coverage for the German workforce.

Income-based contributions: Your monthly payments are determined by your earnings, but there’s a cap to ensure fairness.

Private Health Insurance in Germany (PKV):

Customized Premiums: With the PKV, your premium is uniquely tailored based on age, health history, and chosen benefits.

Flexible coverage: This option allows for more personalised plans, accommodating those who want treatments like alternative medicine or premium hospital care.

What about health insurance for part-time self-employed freelancers in Germany? Even if you freelance on the side, your primary job’s insurance setup has got you covered.

Before choosing between the public (GKV) and private (PKV) health insurance options, consider the long-term implications. Initial savings from the PKV for younger professionals can shift to higher costs in later years. So it’s important you take an informed decision.

| Age | Public Health Insurance (14% of Income) | Private Health Insurance (Minimum Coverage) | Private Health Insurance (Premium Coverage) |

|---|---|---|---|

| 26 years old | €198 – €918 | €223 – €859 | Higher than €859 |

| 56 years old | €198 – €918 | €503 – €1,402 | Higher than €1,402 |

| Aspect | Private Health Insurance | Public Health Insurance |

| Cost Factors | Age, coverage level, pre-existing conditions | Income, contributions based on total earnings |

| Cost Flexibility | Premiums based on chosen coverage and services | Contributions may vary based on total income |

| Tax Deductibility | Premiums partially deductible as business expenses | Contributions fully deductible as business expenses |

| Income Dependency | Not directly tied to income | Contributions based on total earnings |

| Age-Based Premiums | Premiums may increase with age | Not affected by age |

| Coverage Customisation | Customizable coverage options | Standardized coverage provided |

| Switching Difficulty | Can be challenging to switch back to public | Switching to private insurance is more flexible |

| Healthcare Providers | Wide network of private healthcare providers | Limited to providers within public network |

| Eligibility Criteria | Based on self-employed status and income | Requires certain employment history and income |

No, private health insurance for self-employed persons is not inherently more expensive than public insurance. Especially with a moderate to high annual income, the private option could be more cost-effective.

To voluntarily enter public health insurance when self-employed, you must have been insured under public insurance for at least two out of the last five years or have been insured before starting your self-employment.

The costs are based on your earnings, including all sources of income. The contributions can be deducted from taxes since self-employed individuals pay higher contributions compared to employees.

Switching from public to private health insurance is possible, but there are specific requirements. You must be under 55 years old, meet a certain income threshold, and not have been insured under public insurance for the past five years. Reverting back to public health insurance comes with certain challenges.

Here is an example of when public health insurance may be a favorable choice for self-employed professionals:

Maria is a graphic designer. She is considering her health insurance options as she becomes self-employed. Let’s examine why Maria might choose public health insurance over private insurance in this case:

1. Income level: Maria’s income is relatively low, especially during her first years of self-employment. Public health insurance premiums are calculated based on income, which means that Maria’s contributions will be proportionate to her earnings. Private insurance, on the other hand, generally charges premiums based on factors like age and health status, and they tend to be higher, making them less affordable for individuals with lower incomes.

2. Stability and predictability: Public health insurance is more stable and predictable because it is based on income and are subject to a cap. In contrast, private insurance premiums can increase significantly with age.

3. No discrimination based on health: Public health insurance cannot deny coverage or charge higher premiums based on pre-existing health conditions.

4. Family considerations: If Maria has a family, public health insurance often provides family coverage at no extra cost. Private insurance policies usually require separate premiums for each family member.

5. Flexibility: If Maria’s income fluctuates, her public health insurance contributions will adjust accordingly. So she can continue to afford health insurance even during periods of lower income.

It is important to have a set-up for bookkeeping and taxes as a self-employed professional.

Whether you’re a freelancer, a business owner or a Kleinunternehmer, with Accountable you track, manage, and file your taxes with ease. The Accountable software even guarantees error-free tax returns: In the case of errors due to Accountable, we will refund resulting back taxes up to 5,000€.

What you can do with Accountable:

Do you have further questions about self-employment? Simply send us a message with your questions and receive a free and personalised answer from our tax coaches.